You might be feeling it’s an odd title given CNX Nifty (which consists of India’s top 50 companies) is merely 3.7% below its all-time high of 11,171, hit in Jan 2018.

Median drop in Nifty 50 Stocks from their 52-week high though is 17%, but the index is holding up thanks to a few heavyweights like HDFC Duo & Reliance hitting lifetime highs.

But what about broader markets?

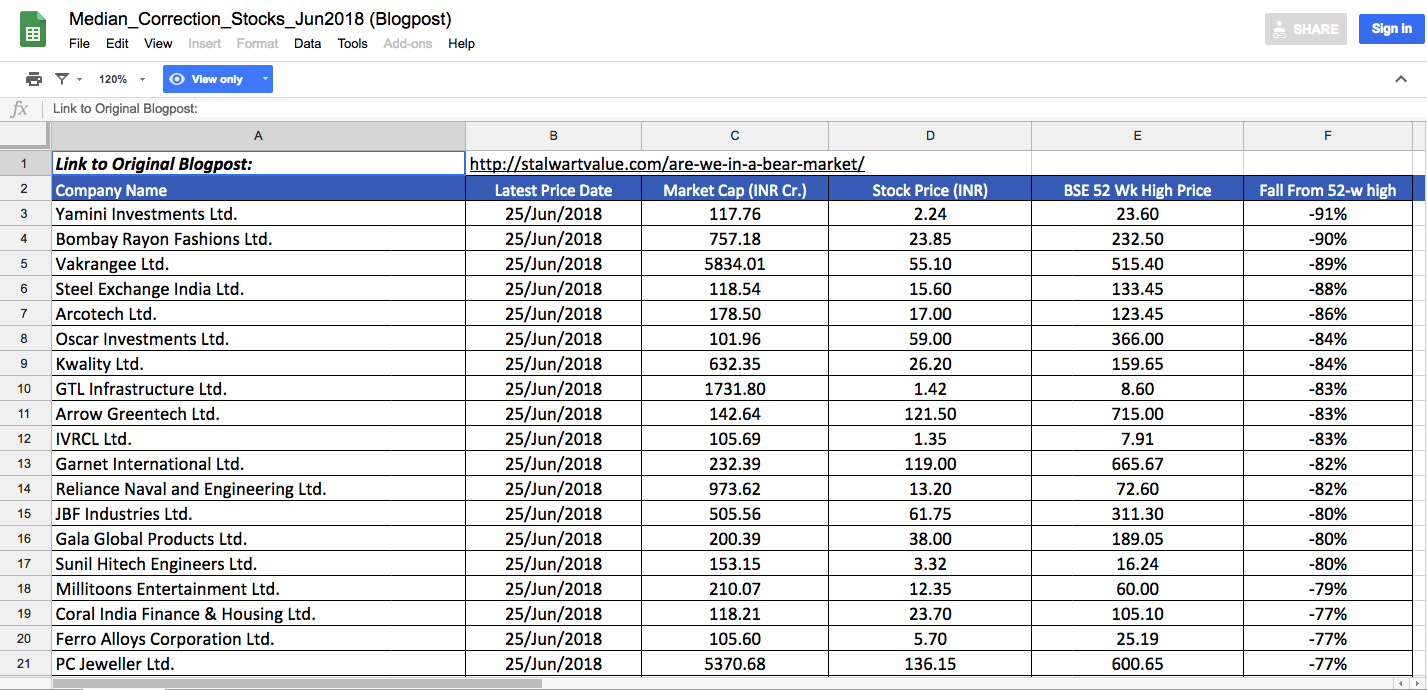

Following is some eye-popping performance data about the 1,584 stocks listed on BSE with a market capitalization of more than Rs 100 Cr. as on 25th June 2018:

| Fall from 52-week high (Source: Ace Equity, Stalwart Advisors Research) | No. of Stocks |

|

>= 60% |

106 |

|

50% – 59% |

175 |

|

40% – 49% |

289 |

| 30% – 39% |

359 |

| 20% – 29% |

336 |

The median fall for these 1,584 stocks from their 52-week high is 34%.

See the complete list along with workings here: Google Sheet

Hence, the Nifty is not at all reflecting the reality of broader markets. It might already be a bear market for many micro, small and mid-cap stocks. Many of these stocks may not see those astronomical prices again, till at least the next bull market, that is only if they manage to survive till then.

What led to this?

We have had a fantastic run up over the last few years. Especially 2017 was a spectacular year in terms of returns. However, as we entered 2018, valuations were stretched and markets probably were looking for a reason to correct. It got plenty of them, starting with re-introduction of LTCG, followed by a series of auditor resignations and alleged fraud in companies like Vakrangee and Manpasand making headlines & dampening the sentiment. Then there was the stock classification rejig by SEBI for Mutual Funds wherein a lot of small & mid-cap stocks held by so-called ‘large-cap’ mutual funds had to be sold in order to comply with new regulations.

What is our take?

Throughout 2017 we had been cautioning about stretched valuations and advising to go defensive (read the memo and blog posts annexed at the end).

The on-going correction has taken out a lot of froth however the valuations are still not ‘mouth-watering’, at best they can be called ‘reasonable’. Next 12 months are mostly going to be about the 2019 elections with the government’s focus shifting to populist measures from infrastructure development & policy reforms, while investors might stay concerned about the outcome. Though history shows that over longer time frames, there hasn’t been a strong correlation between market returns and any specific government. Over last 30 years, average equity returns have been healthy irrespective of whether we had a clear majority or a coalition, an NDA or a UPA.

While it is always difficult to predict short-term market moves, we are not very bullish over the next 12 months and expect the market to be range-bound, barring some stock-specific opportunities which look promising and may yield good returns even in this period.

How should one move forward?

One should stay cautious and focus on safeguarding the gains made over last few years. Unlike 2017 where everything went up, 2018 and 2019 will be much more stock-specific and one has to focus more on bottom-up. Incrementally, we suggest focussing more on large caps versus small/mid caps. Individual investors often ignore large caps thinking they are well discovered and hence not rewarding, which is not entirely true. There is a long list of large caps including HDFC Bank, Maruti, Eicher, Bajaj Finance etc. which despite being discovered for so long have created consistent wealth for shareholders.

One strategy which we prefer while investing in large caps is to go contrarian (read blog post annexed at the end of this post); when you take out brokerage reports on a business and most of them are negative, that’s the time to look at it. You don’t have to be a contrarian for the sake of it, rather you have to then try to understand the business better than others and look for green shoots. You generally get such opportunities at very attractive valuations as nobody is interested in them. Mahindra Finance and Crompton are few such investments we made in the last couple of years and made 100% return on each in a short period of time as the pendulum shifted from extremely negative to positive.

During such uncertain times, those sitting with idle capital may also hunt for opportunities in special situations like demergers. We have added two such large positions in our portfolio recently, where we expect major value unlocking via demerger.

This is the testing time to see how resilient one’s portfolio is and whether business and management are truly high quality.

Annexure:

- [Memo] A Note from CEO – View on Current Markets & Portfolio Strategy (Aug 2017)

- ‘Growth Investing’ Vs ‘Growth Revival’ – Which style to follow? (Dec 2017)

- Blog Post – Investing Mantra for Large-Caps – Go Contrarian (Case Study) (Apr 2018)

- Click here to access Google Sheet with the complete list of stocks and workings:

Leave a Reply